A History of Money: From Cowrie Shells to Bitcoin

Why barter is a myth, how China invented banknotes, and what a stone at the bottom of the sea has in common with a blockchain

Take a banknote out of your wallet. It's printed paper that costs a few cents to make. Yet it will buy you lunch, a book, or an hour of another person's work. Why? Because we all believe it works. And that belief — what we extend it to, whom we give it to, and why — is the main character in a story that stretches across five thousand years of human history.

It's a story full of surprises. Because it begins nothing like the way they taught you in school.

The myth of barter: how it (didn't) begin

The classic textbook tale goes like this: first, people swapped goods for goods. The cobbler needed bread, the baker needed shoes, and when the two happened to meet, they shook on it. But what if the baker doesn't need shoes? This inconvenience — economists call it the double coincidence of wants — supposedly pushed humanity to invent money. Adam Smith was telling this version as far back as 1776, and almost every economics textbook has repeated it ever since.

There's just one catch: anthropologists have never found a single society that actually worked this way.

The Cambridge anthropologist Caroline Humphrey summed it up in 1985 in a sentence still quoted today: "No example of a barter economy, pure and simple, has ever been described, let alone the emergence from it of money." Out of the thousands of societies ethnographers have studied over the past two centuries, the number that ran on pure barter is exactly zero. In his book Debt: The First 5,000 Years (2011), the anthropologist David Graeber adds that economics simply invented a barter prehistory that never existed. The reality, he says, looked different: people in small communities lived on debts and obligations. Your neighbor gave you a cow, knowing that when he needed something himself one day, you'd return the favor. Money as "something that passes from hand to hand" wasn't needed for a long time.

The earliest evidence of money fits this picture. It isn't coins, but bookkeeping: cuneiform tablets from Mesopotamian temples and palaces (Uruk, ~3300–3000 BC), where scribes kept records in a unit called the shekel — originally a measure of weight (about 8.3 grams of silver, with a fixed conversion into barley). The Code of Hammurabi (~1750 BC) sets out fines and payments in shekels of silver. Silver by weight functioned as money here more than a thousand years before coins were invented — and this first money grew out of bureaucracy, not the marketplace.

In fairness, some economists (George Selgin, for one) counter that we know nothing about the era before written records, so Graeber's conclusion is also just a hypothesis. But no one disputes the ethnographic fact — the barter paradise is a myth.

Commodity money: shells, cattle, and salt

Once a community outgrew the circle of familiar faces, it helped to have something everyone would accept. The ideal candidate is durable, portable, divisible, and hard to counterfeit. And so, in various corners of the world, all sorts of things became money — grain, cattle, salt, cocoa beans, cloth… and, above all, shells.

Cowrie shells are small, glossy, practically indestructible, and impossible to fake. One species is even named Monetaria moneta — literally "money cowrie." They served as currency in China as early as 1200 BC, circulated in parts of Africa well into the 19th century, and the Chinese characters for words like "buy," "sell," and "wealth" still contain a shell component (貝). When shells ran short, the Chinese began casting them from bronze — and these bronze imitation cowries are, in effect, among the first metal money in the world.

We still carry traces of commodity money in our language. The Latin pecunia (money) comes from pecus — cattle. And the word salarium (the source of the English salary) was already linked to salt by Pliny the Elder — though the tale that Roman legionaries were literally paid in salt isn't backed by any direct sources.

The rai stones: a Stone Age blockchain

The strangest commodity money in the world is found on the Micronesian island of Yap: enormous limestone discs called rai, with a hole in the middle, some of them heavier than a car. The specimen at the Smithsonian weighs 76 kilograms — and it's one of the smaller ones.

The stones weren't used to buy the daily catch of fish. They were reserved for important payments — marriage settlements, ceremonies, politics. And since nobody wanted to haul a multi-ton stone anywhere, ownership was transferred by verbal agreement before the community. The stone stayed exactly where it stood; all that changed was the shared record of whose it was.

The best story was recorded by the ethnographer William Henry Furness (1910) from local accounts: one family's stone sank to the bottom of the sea while being ferried across. And you know what? Nobody minded. Everyone knew the stone still existed down there, so the family stayed "wealthy" — thanks to a stone no one ever saw. The economist Milton Friedman wrote a famous essay about it in 1991, The Island of Stone Money. And if that reminds you of a ledger nobody holds in their hands but everyone trusts… hold on to that thought. It comes back at the end of the article.

The first coins: Lydia, c. 630 BC

Coins — a piece of metal with a guaranteed weight and the stamp of an authority — appeared in Lydia, a kingdom in western Anatolia (today's Turkey), in the second half of the 7th century BC, roughly around 630 BC. The oldest documented specimens were found by British Museum archaeologists in 1904–1905 beneath the Temple of Artemis at Ephesus: 93 coins of electrum, a naturally occurring alloy of gold and silver that the Lydians panned from the river Pactolus.

Here comes the detail I love most in this whole history. Modern analyses have shown that Lydian coins weren't simply remelted river electrum. Natural Anatolian electrum contains 70–90% gold, yet the royal coins from Sardis have a gold content carefully controlled at 55% ± 2%, with a touch of copper for color and hardness. So the Lydians deliberately diluted the alloy with silver — and a coin bearing the king's seal (a lion) carried a face value higher than its metal warranted. The difference, roughly 15–20%, was the state's profit. It's called seigniorage, and governments still feast on it today. The first coin in history was at the same time the first currency whose value rested on trust in an authority, not on metal alone.

The last Lydian king, Croesus ("rich as Croesus" — yes, that one), then replaced electrum around the middle of the 6th century BC with two parallel series of coins struck from pure gold and pure silver — the first bimetallic system. Herodotus wrote of the Lydians that they were "the first of all men whom we know who coined and used gold and silver currency." The idea proved viral: the Greek city-states adopted it within a few decades. Coins seem to have arisen independently in China too (at roughly the same time) and later in India — though historians still argue over the dating and the degree of independence of the Indian issues.

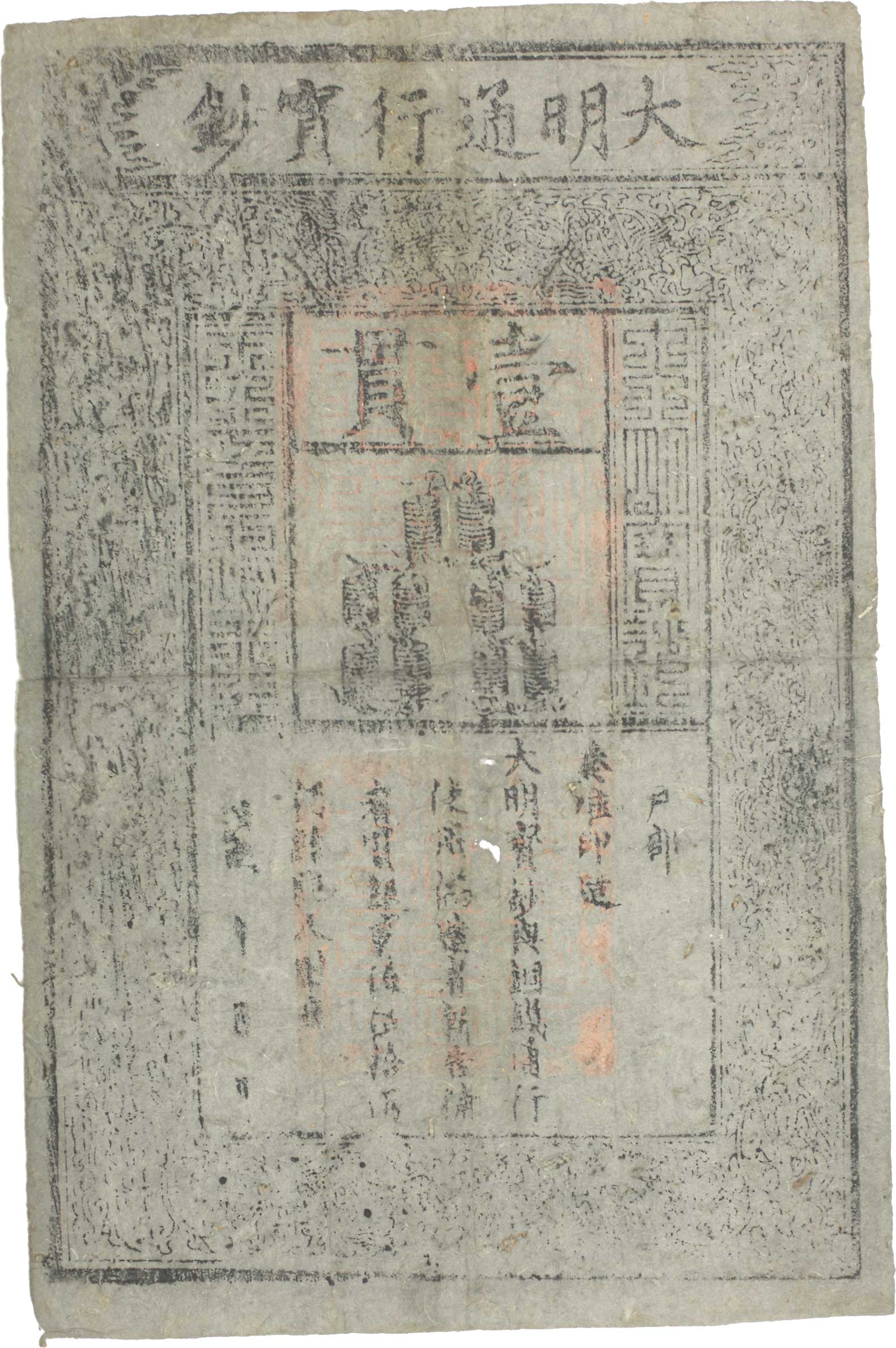

Paper money: a Chinese invention with a bitter ending

Europe had to wait for the next revolution — and, just as with paper, gunpowder, and printing, China got there first.

Tang-dynasty China (9th century) already knew "flying money" (feiqian) — bills of exchange that spared merchants from hauling cartloads of bronze coins across half the empire. Real banknotes were born in Sichuan: there, around the year 1000, private merchants began printing paper vouchers called jiaozi, and in 1023 the Song-dynasty state took over their issue, setting up in Chengdu the first government paper-money office in history.

The Venetian Marco Polo saw the paper money of Mongol Yuan China two and a half centuries later, and back home nobody wanted to believe him: a scrap of paper stamped with the Khan's seal supposedly worked like gold, and anyone who refused to accept it risked death. Notice the definition — money by official decree, enforced by the state. The Chinese tried out fiat currency many centuries before Europe. Including its characteristic failure: sooner or later, every dynasty gave in to the temptation to print more.

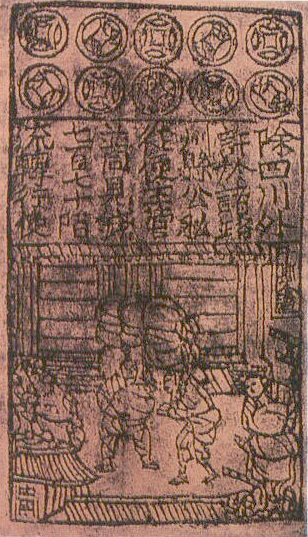

The Ming banknote Da Ming Baochao from 1375 was worth 1,000 bronze coins — it even has them printed in the middle, ten strings of a hundred, so that anyone who couldn't read would know what they were holding. But the state printed and printed, the notes lost most of their value, and by the mid-15th century China effectively abandoned paper money and went back to silver. The first great experiment with paper ended, after more than four centuries — in inflation.

Europe replayed the Chinese script almost to the letter: the first European paper money was issued by Stockholms Banco, Johan Palmstruch's bank in Sweden, in 1661. The bank issued more notes than it had backing for, collapsed within three years, and Palmstruch was sentenced to death (the sentence was ultimately commuted to prison). You already know this pattern.

The thaler: a Bohemian ancestor of the dollar

A small Czech aside, because this really ought to be in bold in the history books. In 1520, the Bohemian Diet granted the Counts of Schlick the right to mint a large silver coin from a rich local deposit in Jáchymov (in German, Joachimsthal) — trial strikes had probably been running a year earlier. It was called the Joachimsthaler, shortened to thaler, in Czech tolar. The coin spread across Europe, was known in Dutch as the daalder, and when the word reached the American colonies, it was garbled into… dollar. So the next time you see the $ sign, know that it was born in the Ore Mountains.

The gold standard: money on a leash

Metal coins have a natural ceiling: an economy can grow faster than silver can be mined. Paper, meanwhile, tempts you to print. The 19th century tried a compromise — paper firmly tethered to gold.

Britain declared gold the sole standard of value with the Coinage Act of 1816, which introduced the gold sovereign, and the system ran at full tilt from 1821, when the Bank of England resumed the convertibility of its notes into gold. By the end of the 19th century, practically every major economy had joined; the United States did so definitively with the Gold Standard Act of 1900. A banknote was a claim check on gold: a set number of grams of the precious metal, on demand. The result was a long era of price stability and explosive growth in world trade — but also a system that couldn't respond flexibly to crises. When war or panic hit, states simply suspended convertibility.

The Great Depression broke the gold standard's back. In April 1933, President Roosevelt's Executive Order 6102 ordered Americans to surrender — bar a few exceptions — their gold coins, bullion, and gold certificates in exchange for paper dollars. The Gold Reserve Act of January 1934 then authorized the president to devalue, and the official price of gold rose from 20.67 to 35 dollars per troy ounce. The dollar was thereby devalued overnight by 41% — and private ownership of monetary gold was banned (the ban wasn't lifted until 1974).

Bretton Woods: gold for the chosen few

In July 1944, while the war was still on, delegates from 44 Allied nations gathered at the Mount Washington Hotel in Bretton Woods, New Hampshire, to design a postwar monetary order. (The conference was called the "United Nations Monetary and Financial Conference" — "United Nations" here meant the wartime Allied coalition; the UN itself wasn't founded until a year later.) The result: the currencies of member states pegged firmly to the dollar (within a ±1% band), and the dollar pegged to gold at 35 dollars an ounce. The International Monetary Fund was created (formally on 27 December 1945, with 29 countries signing), and the system became fully operational in 1958, when the European currencies restored convertibility.

The catch: gold could no longer be claimed by a private citizen, only by foreign governments and central banks. The whole world thus rested on America's promise to back its dollars with gold whenever asked. But dollars kept piling up abroad (the Marshall Plan, Vietnam, domestic deficits) — until there were more of them than there was gold sitting in Fort Knox. The system had turned into a run on the bank, only in slow motion and on an international scale.

15 August 1971: the day money stopped being backed

Over the weekend of 13–15 August 1971, Richard Nixon summoned fifteen advisers to Camp David — among them Fed Chairman Arthur Burns, Treasury Secretary John Connally, and Paul Volcker. On Sunday evening, he announced his "New Economic Policy" on television: a 90-day freeze on wages and prices, a 10% surcharge on imports, and — almost in passing — a "temporary" suspension of the dollar's convertibility into gold.

The word "temporary" is one of the running jokes in monetary history. The gold window never opened again. An attempt to fix exchange rates without gold (the Smithsonian Agreement, December 1971) held only briefly; since March 1973 the currencies of the major economies have floated freely, and the Jamaica Accords (1976) merely rubber-stamped the end of gold in the monetary system.

Since 1971, then, we've been living in the era of fiat money (from the Latin fiat — "let it be," "let it become"): money backed by nothing but a state's decision and the trust that the central bank won't abuse the money supply. This isn't necessarily a disaster, as the popular shorthand claims — a flexible monetary policy can cushion crises (2008 would have looked worse under a gold standard), and solid central banks keep inflation more or less in check. But the safeguard is missing from the system, and history supplies, with iron regularity, vivid examples of what happens when a state lets the printing press off the leash: Weimar Germany in 1923 (at the peak of the crisis, prices doubled roughly every four days, and by November a dollar cost 4.2 trillion marks), Hungary in 1946, Yugoslavia in 1994, Venezuela…

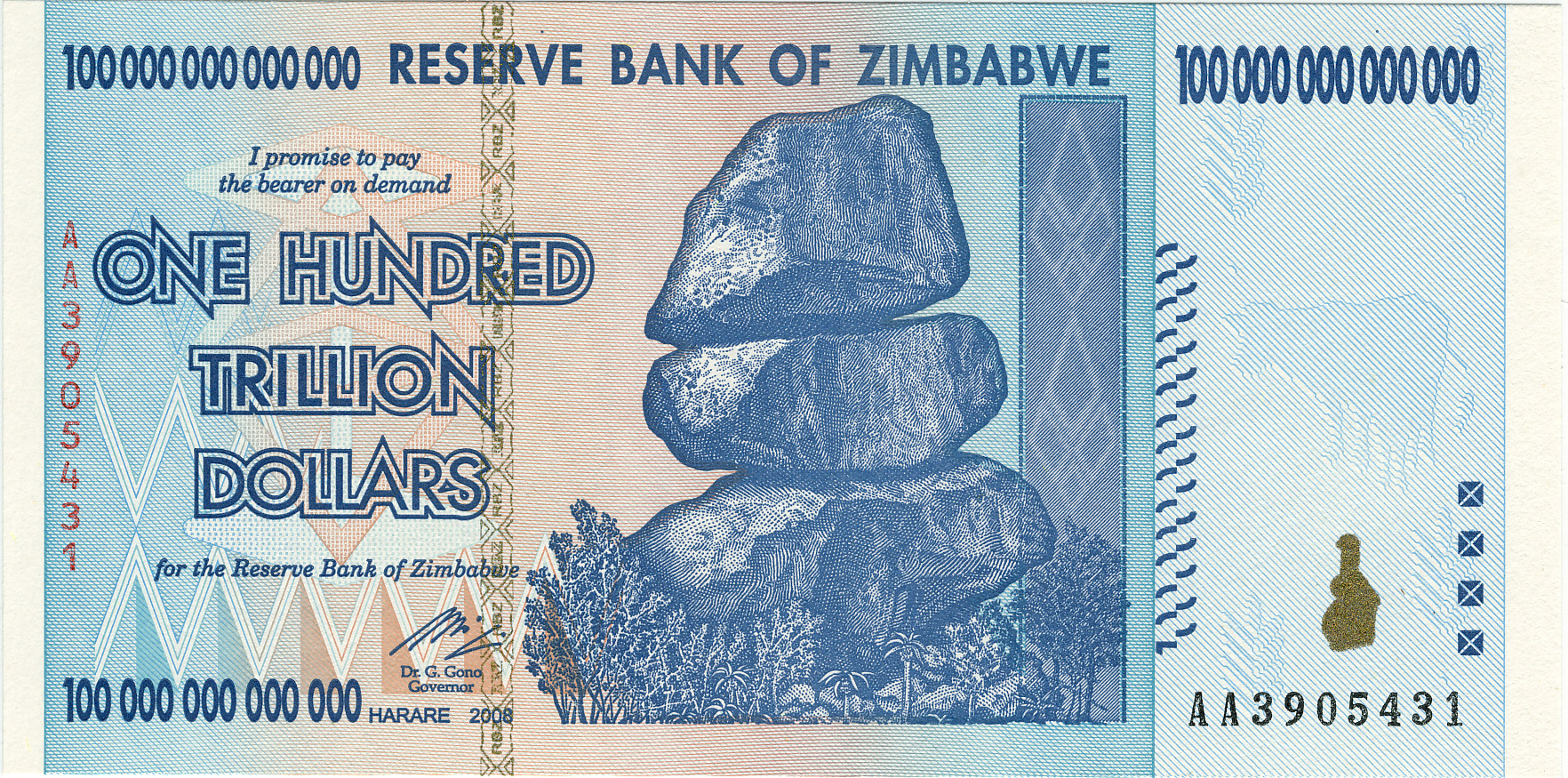

The modern record-holder is Zimbabwe: in November 2008, year-on-year inflation there reached an estimated 89.7 sextillion percent (a number with more than twenty zeros), according to the economist Steve Hanke, and in January 2009 a hundred-trillion-dollar banknote appeared — the highest denomination of the 21st century (the all-time record belongs to a Hungarian hundred-quintillion-pengő note from 1946). It bought you, at best, a bus ticket. A few months later, the currency ceased to exist.

Bitcoin: an attempt at money without trust in the state

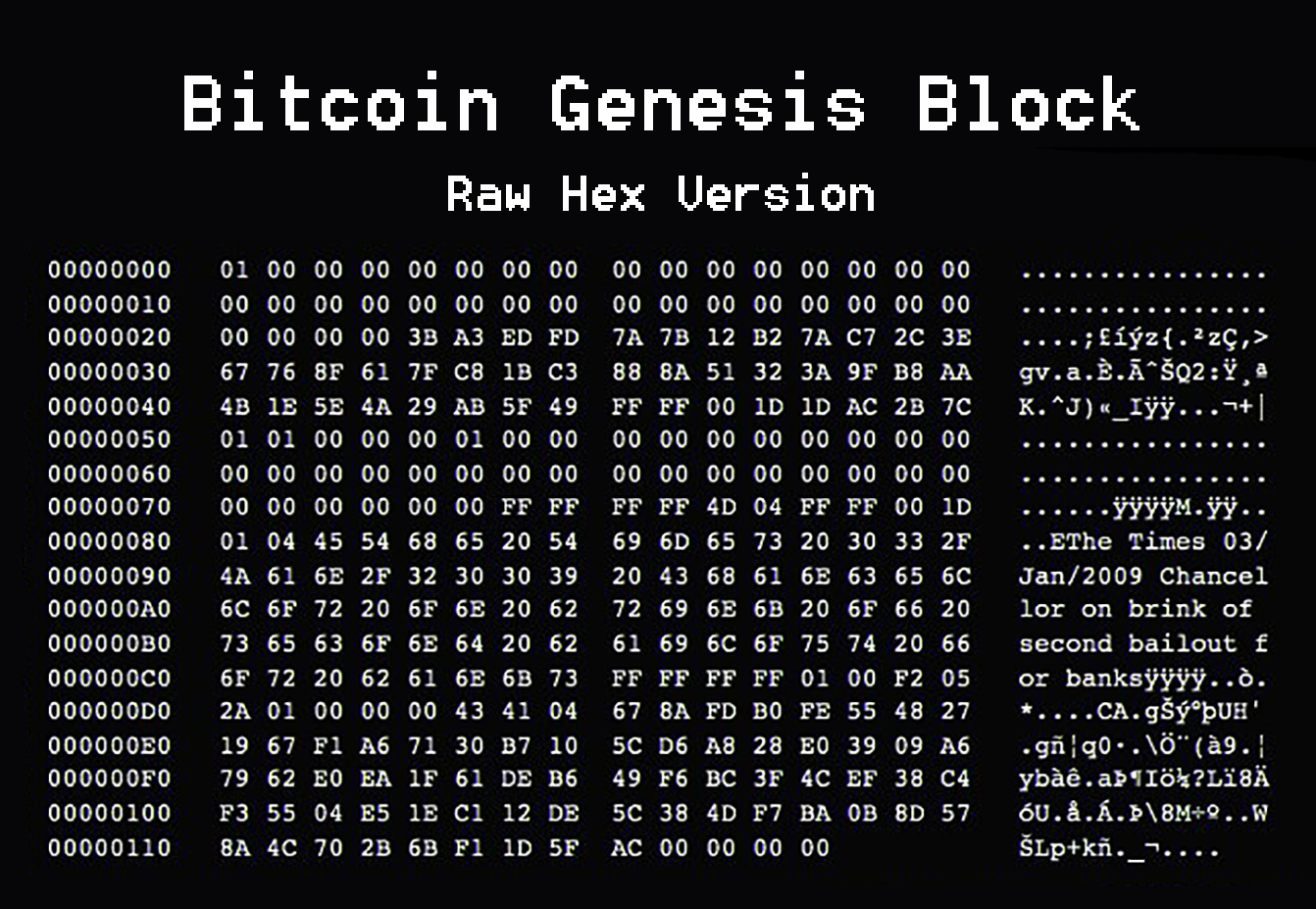

And then came October 2008. The world was tumbling into the biggest financial crisis since the 1930s, governments were bailing out banks with taxpayers' money — and on 31 October 2008, someone under the pseudonym Satoshi Nakamoto sent a nine-page PDF to a cryptography mailing list: Bitcoin: A Peer-to-Peer Electronic Cash System. Who it was, no one knows to this day.

On 3 January 2009, Nakamoto mined the first block of the Bitcoin blockchain. And into its guts he wrote a message that is at once a timestamp and a manifesto — that day's headline in The Times of London:

"The Times 03/Jan/2009 Chancellor on brink of second bailout for banks"

Nine days later, on 12 January 2009, the first transaction between two people took place: Nakamoto sent 10 BTC to the cryptographer Hal Finney. And on 22 May 2010 came the first documented purchase of physical goods — the programmer Laszlo Hanyecz paid 10,000 BTC for two pizzas. (No, we won't calculate what those pizzas would cost today. Laszlo is banned from doing that too.)

What's new about Bitcoin from the vantage point of five thousand years of monetary history? Three things:

Scarcity without metal. The protocol sets a cap of 21 million coins. The reward for a mined block started at 50 BTC and halves every 210,000 blocks (roughly every four years) — since April 2024 it's 3.125 BTC. It's the first case of digital scarcity: "gold" whose supply everyone knows a hundred years in advance.

A ledger without an accountant. There's no central authority you have to trust; transactions are verified by a network of thousands of independent computers, and the record is public. Remember the island of Yap? The stone lay at the bottom of the sea, but everyone knew whose it was — because ownership was a record in the community's collective memory, not a matter of physical possession. Bitcoin is that same principle taken to its software conclusion. (Friedman missed his "stone money in digital form" by only a few years.)

Money as opt-in. For the first time in the modern era, there's a currency no state issues, enforces, or is able to switch off. Whether that's a feature or a bug is a question the world hasn't settled — El Salvador made bitcoin legal tender in 2021, only to scrap the mandatory-acceptance requirement in 2025 under a deal with the IMF. The experiment is running.

Over its seventeen years of existence, Bitcoin has traveled from a curiosity for cryptographers, through the currency of darknet marketplaces, all the way to an asset held by sovereign funds and stock-exchange ETFs. Whether it's a new chapter in the history of money or a dead end will be decided — as always in this story — by the trust of enough people.

What five thousand years haven't changed

Run through the story backwards: Bitcoin is a record in a distributed database. The fiat dollar is a record in a central bank's database. The gold certificate was a paper record of gold in a vault. The jiaozi was a record of bronze coins held by a merchant in Chengdu. The rai stone was a record in a village's collective memory. And the shekel of barley was a cuneiform record on a tablet in a temple in Uruk.

Money was never a thing. It was always a record of trust — and the various eras differ mainly in who keeps that record and how easily it can be faked. Shells and gold were guarded against forgery by nature itself — through scarcity. Kings gave in to the temptation of seigniorage. States are watched by… well, nobody, really, which is why it occasionally ends up like Zimbabwe. Bitcoin is testing whether mathematics can do the job.

So the next time you tap your card against a terminal — no coin, no paper, just a few numbers rewritten in the databases of two banks — remember that you're doing exactly what the people of Yap did with a stone at the bottom of the sea. It's just that the community that trusts the record is now a little larger.

Sources

Caroline Humphrey: Barter and Economic Disintegration. Man (N.S.) 20(1), 1985, pp. 48–72. — jstor.org/stable/2802221

David Graeber: On the Invention of Money. — davidgraeber.org

David Graeber: Debt: The First 5,000 Years. Melville House, 2011.

Smithsonian National Museum of American History: exhibition The Value of Money. — americanhistory.si.edu

John H. Kroll: The Coins of Sardis. Sardis Expedition (Harvard/Cornell). — sardisexpedition.org

Austrian Academy of Sciences (OeAW): Early Lydian Coinage and Chronology. — oeaw.ac.at

Jacques Melitz: The reasons for Lydian electrum coins… CEPR VoxEU. — cepr.org

Federal Reserve History: Creation of the Bretton Woods System. — federalreservehistory.org

Federal Reserve History: Nixon Ends Convertibility of US Dollars to Gold. — federalreservehistory.org

U.S. Department of State, Office of the Historian: Nixon and the End of the Bretton Woods System, 1971–1973. — history.state.gov

Milton Friedman: The Island of Stone Money. Hoover Institution Working Paper E-91-3, 1991. — hoover.org

William Henry Furness III: The Island of Stone Money: Uap of the Carolines. Lippincott, 1910.

Marco Polo: The Travels of Marco Polo (Yule–Cordier translation), Book II, ch. XXIV on paper money. — gutenberg.org

Sveriges Riksbank: First banknotes in Europe (Stockholms Banco, 1661). — riksbank.se

Radio Prague International: Predecessor of US dollar minted 500 years ago in Jáchymov. — english.radio.cz

Executive Order 6102 (5 April 1933), full text. — presidency.ucsb.edu

Satoshi Nakamoto: Bitcoin: A Peer-to-Peer Electronic Cash System, 31 October 2008. — bitcoin.org/bitcoin.pdf

Announcement of the whitepaper on the cryptography mailing list, 31 October 2008. — metzdowd.com

Bitcoin genesis block (block 0, 3 January 2009) in a blockchain explorer. — blockstream.info

Steve H. Hanke, Alex K. F. Kwok: On the Measurement of Zimbabwe's Hyperinflation. Cato Journal 29(2), 2009. — cato.org

Images and licenses

All images come from Wikimedia Commons and are freely licensed:

Cowrie shells: Shang Cowrie Money, Gary Todd, CC0

Rai stones: Ancient Yapese stone money, Scot Nelson, CC0

Lydian trite: Electrum trite, Alyattes, Lydia, photo by Classical Numismatic Group, CC BY-SA 3.0

Jiaozi: Jiao zi, public domain

Ming banknote: Da Ming Tongxing Baochao, public domain

Thaler: Joachimsthaler, NTNU Vitenskapsmuseet, CC BY 2.0

Gold certificate: US $50 Gold Certificate 1928, National Museum of American History, public domain

Bretton Woods: Morgenthau Bretton Woods opening 1944, public domain

Zimbabwe: Zimbabwe $100 trillion 2009, Reserve Bank of Zimbabwe, public domain

Genesis block: Bitcoin Genesis block, public domain

Casascius bitcoin: Physical Bitcoin by Mike Cauldwell, Mike Cauldwell, free use

.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

_-_Da_Ming_Tongxing_Baochao_(%E5%A4%A7%E6%98%8E%E9%80%9A%E8%A1%8C%E5%AF%B6%E9%88%94)_Auction_World_07.jpg){kind=link}

.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

.jpg){kind=link}

Was this article helpful?

Comments

No comments yet.